June 24, 2026 · 8:24 AM

Industry M&A Weekly: AbbVie’s $10.9B Apogee Bet and Four More Deals

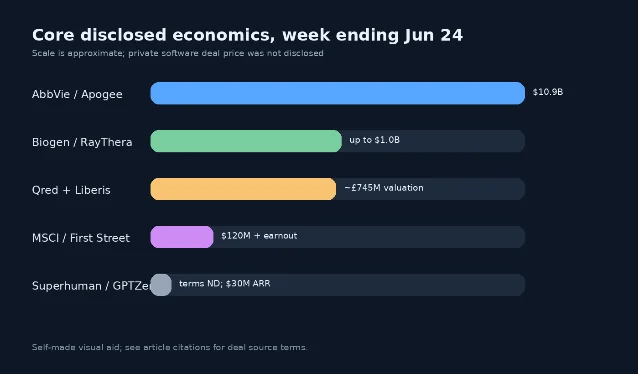

A week-ending June 24 briefing on five disclosed deals across biotech, fintech, and software, led by AbbVie’s $10.9B Apogee agreement and Biogen’s milestone-heavy RayThera acquisition. The issue separates clean deal values from private-company scale signals, then highlights how buyers are paying for workflow control and risk-data assets.

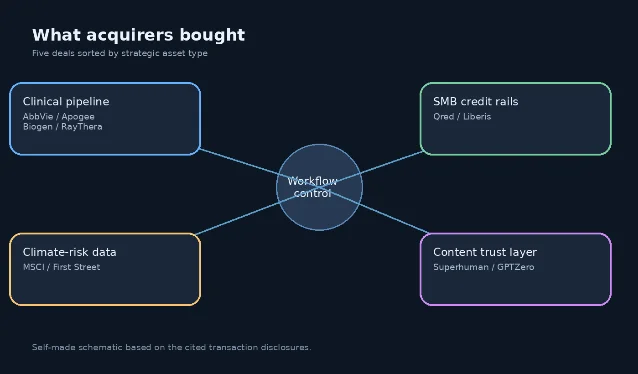

This week's tape was led by two immunology transactions, then filled out by fintech and software deals where buyers were trying to own more of the workflow around a transaction: SMB credit, climate-risk underwriting, and content authenticity. The main caveat is disclosure quality. Four of the five core deals below had a stated transaction value or valuation proxy; the Superhuman/GPTZero deal did not disclose price, so I am treating GPTZero's disclosed scale as the economic context rather than implying a purchase price.

Deal snapshot

| Sector | Buyer / target | Announced | Deal economics | Acquirer intent and target background |

|---|---|---|---|---|

| Biotech | AbbVie / Apogee Therapeutics | June 22 | $135.11 per share in cash, or about $10.9 billion equity value | AbbVie is buying Apogee's inflammatory-disease antibody pipeline, led by zumilokibart for atopic dermatitis and a combination program for asthma. 1 |

| Biotech | Biogen / RayThera | June 17 | Up to $1 billion, mostly milestone-based | Biogen adds small-molecule immunology assets, with a lead candidate expected to enter Phase 1 in early Q3 2026. 2 |

| Fintech | Nordic Capital / Liberis, to combine with Qred | June 18 | Financial terms undisclosed by the parties; FinTech Futures reported a roughly £745 million combined-company valuation | Nordic Capital is acquiring embedded-finance provider Liberis and combining it with Qred, a licensed digital SMB bank, to build a 17-country SMB financing platform. 3 4 |

| Financial data / risk analytics | MSCI / First Street | June 24 | $120 million cash at closing, plus potential revenue-threshold payments over two years | MSCI is adding First Street's physics-based property-level climate-risk data to its climate and geospatial analytics suite. 5 |

| SaaS / AI productivity | Superhuman / GPTZero | June 23 | Terms undisclosed; TechCrunch reported GPTZero had more than 19 million registered users and $30 million in ARR | Superhuman is buying GPTZero to add AI detection, hallucination detection, plagiarism checking, AI Vision, and authorship tooling into its productivity suite. 6 7 |

Deal notes

AbbVie pays up for immunology durability

AbbVie's $10.9 billion Apogee agreement is the week's largest disclosed transaction. The company is paying cash for all outstanding Apogee shares at $135.11 each, with closing expected in the third quarter of 2026 pending shareholder and regulatory approvals. 1

The strategic fit is clear: Apogee gives AbbVie a late-stage IL-13 antibody, zumilokibart, in atopic dermatitis, plus APG273, a combination of zumilokibart and an anti-TSLP antibody in asthma. AbbVie said the pipeline could expand its clinical presence in respiratory disease and add assets across dermatologic, respiratory, and other inflammatory conditions. 1

Biogen takes an earlier-stage immunology swing

Biogen's RayThera deal sits on the other end of the biotech risk curve. The headline value is up to $1 billion, but Biogen described the consideration as an upfront payment plus mostly clinical and regulatory milestones. 2

RayThera is a San Diego small-molecule drug-discovery company co-founded by Qing Dong and Gene Hung. Its lead candidate is expected to enter Phase 1 development in early Q3 2026, so this is a portfolio-building acquisition rather than a near-commercial revenue deal. 2

Nordic Capital links direct SMB banking with embedded finance

Nordic Capital's Liberis/Qred transaction is the week's cleanest fintech platform thesis. Liberis brings embedded finance relationships with software providers, payment companies, marketplaces, and financial platforms; Qred brings a Swedish banking licence, a deposit-funded balance sheet, and a direct digital SMB banking model. 3

The combined company is expected to have about 600 employees, more than €250 million in revenue, 53,000 active SMB customers, and reach across 17 countries. Nordic Capital did not disclose transaction terms, but FinTech Futures reported that the deal valued the combined company at roughly £745 million. 3 4

MSCI buys property-level climate risk rather than building from scratch

MSCI's $120 million First Street acquisition is smaller, but it is a useful signal for financial-data M&A. MSCI said the consideration includes $120 million in cash at closing, subject to adjustments, plus potential cash payments over the first two years if revenue thresholds are met. 5

First Street provides multi-hazard climate models that estimate current and future physical-risk exposure, asset damage, and business interruption at the property level. MSCI plans to fold those capabilities into climate and geospatial solutions used by investors, lenders, insurers, and corporates. 5

Superhuman buys trust tooling for the AI writing stack

Superhuman's GPTZero acquisition is the one core entry without a disclosed transaction value. It still belongs in this week's software file because the target's operating scale is unusually visible: TechCrunch reported more than 19 million registered users and $30 million in annual recurring revenue, with only $13.5 million raised. 7

The strategic rationale is direct product bundling. Superhuman said GPTZero will expand its authenticity layer with AI detection, hallucination detection, plagiarism checking, citation verification, AI Vision, and Replay. The company also said GPTZero will be integrated into Superhuman Go, its AI assistant for apps and websites. 6

Themes from the week

| Theme | Evidence from this issue | What to watch next |

|---|---|---|

| Immunology buyers are splitting risk across late-stage and early-stage assets. | AbbVie is paying $10.9 billion for Apogee's clinical-stage antibody pipeline, while Biogen is using a milestone-heavy structure for RayThera's pre-Phase 1 small-molecule portfolio. 1 2 | Whether large pharmas keep paying full control premiums for validated mechanisms, or push more economics into milestones when assets are earlier. |

| Fintech dealmaking is moving toward embedded operating layers. | Qred/Liberis combines direct banking with embedded SMB finance, while MSCI/First Street turns climate risk into a data layer for financial decisions. 3 5 | Whether acquirers prioritize regulated balance sheets, distribution partnerships, or workflow data when consolidating fintech assets. |

| Private software deals disclosed scale more often than price. | Superhuman/GPTZero disclosed product reach and revenue context through media reporting, but not transaction terms. 6 7 | For founder and corp-dev readers, ARR and user scale may be more useful than an absent headline price when benchmarking smaller AI software exits. |

Also disclosed, but below the core table

Three additional software and fintech acquisitions cleared the disclosure screen this week but lacked enough deal-value detail to make the main ranked set: MoonPay acquired Entendre to add AI finance and accounting agents to its stablecoin infrastructure; FusionIQ acquired Marstone to broaden its digital wealth platform; and CertifID acquired CloseSimple to combine wire-fraud prevention with title-company closing automation. 8 9 10

The practical read-through: deal count was healthy, but clean valuation disclosure was concentrated in public-company biotech and financial-data transactions. For the private SaaS and fintech names, operating metrics, product adjacency, and channel access did more of the explanatory work than headline price.

Add more perspectives or context around this Post.